Payments on account – what are they?

A question that new clients ask every year is just what is a ‘payment on account.’ They can be a real challenge to get your head around but in this guide we walk you through everything you need to know.

In simple terms ‘payments on account’ refers to upfront payments you make towards your Self Assessment tax return.

You’re required to make two advanced payments each year towards your tax bill. The only exception to this is if on your last Self Assessment bill you owed less than £1,000 or where 80% or more of your tax bill had tax deducted at source i.e. through PAYE.

Payment on account can be a bit of a head-scratcher and can leave small business owners feeling confused but it’s an important concept to get to grips with! Why? Because not understanding payment on account means you could be presented with a large bill, which if not planned for, you could struggle to pay, leading to late payment penalties.

If HMRC are also expecting a payment on account from you, then not paying this is likely to result in interest, which is another cost to consider.

We go into more detail below.

Payment on account – an example

In the UK, the tax year for a Self Assessment tax return runs from 6 April – 5 April. So, tax year 2021/22 starts on 6 April 2021 and ends on 5 April 2022.

The Self Assessment filing deadline i.e. the latest you need to submit your tax return is midnight on the 31 January, so using the dates above, would be 31 January 2023.

The first time an individual completes a Self Assessment tax return they are unlikely to be required to make payments on account. So, for example, if you completed your first ever tax return for 2021/22 then you won’t have made payments on account for that year.

This means, you need to pay all your tax as normal for this first year on 31 January 2023.

However, this is where things can get complicated…

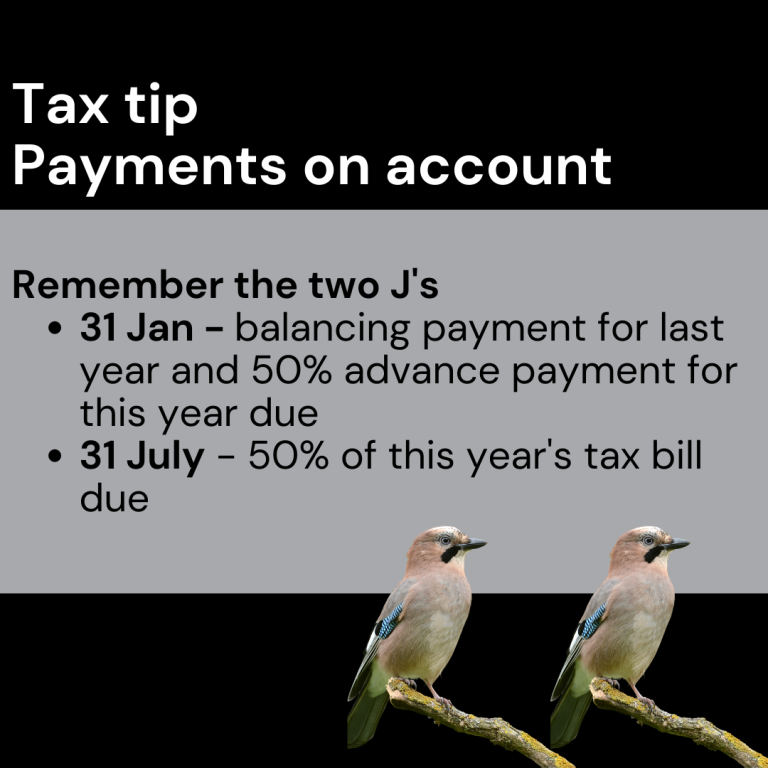

On the 31 January you will also be required to make a payment on account for 50% of your expected tax for the current tax year 2022/23. Meaning, yes that first payment you make could be larger than you’d prepared for! How much larger? Well it could be 50% more than you were expecting!

You then need to make a second advance payment for the remaining 50% of your expected tax for tax year 2022/23 and this will be due on 31 July.

How do HMRC calculate the payments on account due?

You’ll notice we said that you’re required to make two payments each for 50% of your expected tax liability.

Well, just how is this expected liability calculated?

Broadly, the 50% is based on your tax liability for the previous year, so in our earlier example if your liability for 2021/22 was £10,000 then your advance payments on account for 2022/23 would be two payments of £5,000 on 31 January 2023 and 31 July 2023.

So, what happens when you submit the tax return for 2022/23?

So far, you’ve made two advance payments on account towards your 2022/23 tax bill but you may not have actually prepared your self assessment tax return yet. This is because it isn’t due until 31 January 2024.

Because your payments on account are just an ‘expected’ amount when the 31 January 2024 rolls around again you may well have a balancing figure to pay or you may be due some money if you’ve paid more through advanced payments than your final tax bill.

For example, if the tax bill for your second year was £12,000 (£2,000 more than it was in 2021/22) you’ll have to pay the difference of £2,000 on 31 January. That said, if it’s lower, say £8,000 (£2,000 less than 2021/22) you’ll be due £2,000 back from HMRC.

So, if we work on the assumption you’re tax bill for your second year was £12,000 (£2,000 more than it was in 2021/2022) you’d be correct in thinking you’d have a £2,000 balancing payment to make AND you’d be need to make your first expected payment for tax year 2023/2024 – yes, this would be £6,000 (50% of the previous tax year’s bill). You can see how the cycle continues…

Additional FAQs regarding payments on account

Why do HMRC ask for payments on account?

In short, the reason HMRC ask for these advanced payments on account of your expected tax is to prevent debt accruing. The expected tax bill amount for the current year being split into two payments means large, late arrears are less likely to occur.

How to reduce payments on account?

It is possible to reduce your payment on account where you expect your tax bill for the current year to be less than the previous year’s tax bill. In this case, you can request a reduction by including it in your self assessment tax return. Alternatively, if your tax return has already been submitted you can reduce your payments on account via your Government Gateway account.

Where do you go to make payments on account?

There are lots of ways to make a payment on account payment to HMRC. You can do this via bank transfer, Direct Debit and through your Government Gateway account. Check out the full list of options here.

Want support with payments on account?

We’ve got you covered, at Raw we’re practiced at supporting clients with their Self Assessments and can help make the process smooth and pain free. Contact us today.